MDDP

Senatorska 18a

00-082 Warsaw

tel. (+48) 22 322 68 88

biuro@mddp.pl

BARTOSZ GŁOWACKI

Partner | Tax Advisor

Email: bartosz.glowacki@mddp.pl

Mob.: +48 603 980 382

author of the study

NAVIGATION

Rates of selected taxes in Poland

Rates of selected taxes in Poland | |

ITC | 19% (basic rate) |

9% (preferential rate) | |

Minimum CIT | 10% |

Exit tax | 19% |

Tax on shifted income | 19% |

WHT | |

dividends | 19% |

Interest | 20% |

Receivables license | 20% |

Services intangible | 20% |

IP BOX | 5% |

Lump sum tax on corporate income | |

For small taxpayers and for taxpayers starting their business | 10% |

Others taxpayers | 20% |

Capital Gains Tax | 19% |

Tax liability in Poland

Entities with their registered office or management in Poland pay corporate income tax [ITC] from all of their income, regardless of where it is earned.

Entities that do not have their registered office or management board in Poland are subject to taxation only on income they earn in Poland, unless a double taxation treaty provides otherwise.

Income (revenue) earned by taxpayers in the territory of Poland is in particular considered to be income (revenue) from any type of activity conducted in the territory of Poland, including through a foreign establishment located in the territory of Poland.

Who is a CIT taxpayer?

CIT taxpayers in Poland include, among others, legal entities, limited joint-stock partnerships and limited partnerships with their registered office or management board in Poland, tax capital groups, companies without legal personality with their registered office or management board in another country, if, in accordance with the tax law of that country, they are treated as legal entities and are subject to taxation in that country on all of their income regardless of where it is earned.

What is income under the CIT Act?

There are two main sources of revenue in CIT:

- income from capital gains,

- other income.

Income from capital gains includes, among others, dividends and other income actually obtained from the share in the profits of legal persons and companies that are CIT taxpayers, the value of property received as a result of the liquidation of a legal person or company, income from the sale of shares (stocks) in companies.

Other revenues include, primarily, revenues from operating activities.

Revenue from business activity is revenue due (it does not have to be actually received). Revenue due is generated on the day of delivery of the item, disposal of property rights or provision of the service, including partial provision of the service, no later than on the day of:

- issuing an invoice, or

- settlement of debts.

In other cases, revenues also include money received, monetary values, exchange rate differences or the value of items, rights or other benefits received free of charge or partially for a fee.

In the case of a service billed in billing periods, revenue is generated on the last day of the billing period specified in the contract or invoice (no less than once a year).

With respect to revenues to which the above rules do not apply, it is assumed that the date of revenue generation is the date of receipt of payment.

In addition, the regulations provide for separate sources of revenue and taxation rules, such as minimum tax, tax on shifted income, tax on income of foreign controlled entities, tax on income from buildings.

Costs of obtaining income

Costs of obtaining revenues are expenses incurred in order to earn revenues or maintain or secure a source of revenues. Earning revenues is not a condition for deducting an expense as a cost, unless special regulations provide otherwise.

The regulations do not contain a closed list of expenses that constitute tax costs, but they specify a broad list of expenses that cannot constitute costs of obtaining revenues. These include, among others, expenses for repayment of loans (credits), the amount of interest, commissions and exchange rate differences on loans (credits) increasing the costs of investment during the period of implementation of these investments or the amount of fines and pecuniary penalties imposed in criminal, fiscal penal, administrative and petty offence proceedings and interest on these fines and penalties.

Tax depreciation

Fixed assets produced or acquired and acquired intangible assets and legal rights are subject to depreciation. The basic method of depreciation of fixed assets is straight-line depreciation using depreciation rates specified in the Act. In certain cases, declining balance depreciation is possible. Specific groups or types of fixed assets may be subject to accelerated depreciation or individually determined depreciation.

Intangible assets, depending on their type, are amortized in individually determined periods, with the minimum amortization period ranging from 12 to 60 months, depending on the type of intangible asset.

What is taxed under the CIT Act?

The subject of income tax is income that is the sum of income earned from capital gains and income earned from other sources of revenue. Income is the surplus of the sum of revenues earned from this source of revenue over the costs of earning them.

In some cases, the subject of taxation may also be income (e.g. dividends).

Tax loss

The loss from a source of income in a given tax year may be used to reduce the tax base from that source of income in the following five tax years.

The amount of the deduction in any of these years cannot exceed 50% of this loss. Alternatively, a one-time deduction of the loss (for one tax year) can be made in an amount not exceeding PLN 5 million. In such a situation, the surplus over PLN 5 million is deductible in the remaining years of the five-year period on general principles (i.e. no more than 50% of this surplus in a given tax year).

The regulations do not provide for the possibility of deducting losses retroactively.

What are the CIT rates in Poland?

Basic CIT rates in Poland are:

- 19% of the tax base,

- 9% of the tax base on revenues (income) other than from capital gains in the case of taxpayers whose revenues achieved in the tax year did not exceed the amount expressed in złoty corresponding to the equivalent of EUR 2 converted at the average euro exchange rate announced by the National Bank of Poland on the first working day of the tax year, rounded to PLN 000. Additionally, the taxpayer must meet the conditions to be recognized as a "small taxpayer" - except when it is the first year of conducting business.

Who is the small taxpayer?

A small taxpayer is a taxpayer:

- whose gross sales revenue (including the amount of value added tax due) did not exceed EUR 2 million in the previous tax year, converted at the average euro exchange rate announced by the National Bank of Poland on the first working day of October of the previous tax year, rounded to PLN 1000,

How to determine the tax year?

In principle, the CIT tax year is the calendar year. The taxpayer may choose a tax year other than the calendar year by reporting this in the CIT-8 tax return. Also then, the tax year is the period of the following 12 months. In the event of a change in the tax year, it is possible to extend it once to 23 months.

What does the CIT settlement process look like in Poland?

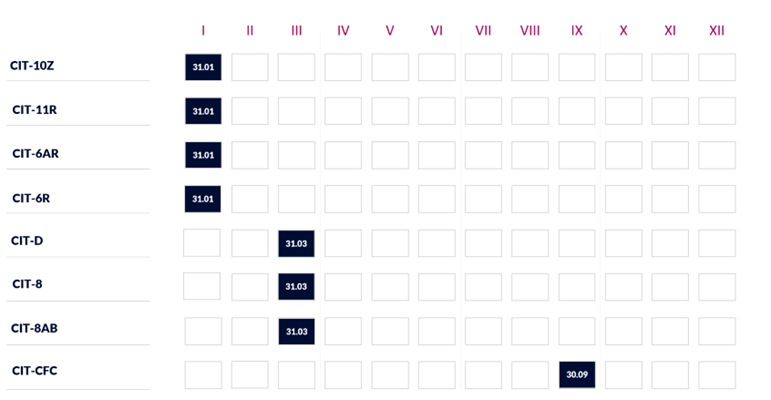

The CIT-8 tax return must be filed once a year. If the taxpayer's tax year coincides with the calendar year, the deadline is March 31 of the following year (if the tax year does not coincide with the calendar year, the deadline is 3 months after the end of the tax year).

Example deadlines for filing CIT tax returns in Poland

*Assuming the tax year is the same as the calendar year.

CIT advances

During the tax year, taxpayers pay monthly advances on the tax due by the 20th day of each month for the previous month.

Taxpayers can also pay quarterly advances. Quarterly CIT advances are paid by the 20th day of each month following the quarter for which the advance is paid. The advance for the last quarter of the tax year must be paid by the 20th day of the first month of the next tax year. This also applies to taxpayers who start a business in the first tax year and for small taxpayers.

Taxpayers can also pay simplified advances, in the amount of 1/12 of the tax due 2 years earlier. If there was no tax to pay for that year, the tax on income from three tax years ago may be taken into account.

What are the penalties for incorrect CIT settlement?

Incorrect settlement of CIT may constitute an act prohibited by the Polish Fiscal Penal Code.

Tax not paid on time becomes a tax arrears, on which interest is charged. Currently, it is 14,5% per annum.

Liability may be borne by, among others:

- a taxpayer who failed to file an annual return on time,

- a taxpayer who filed an annual return but failed to pay the tax due on time,

- a taxpayer who has not filed a tax return and has not paid the tax on time.

In certain cases, only liability is possible. A perpetrator who, after committing a prohibited act, has notified the body responsible for prosecution, disclosing the essential circumstances of the act, in particular the persons cooperating in its commission, is not subject to punishment for a fiscal offence or fiscal misdemeanour. A key element is the prior lack of knowledge of the tax authority about the prohibited act committed.

In addition, it is required to repair the consequences of the prohibited act (paying overdue tax, filing an overdue tax return, etc.).

The legally effective correction of a declaration or book concerning an obligation, the incorrect performance of which constituted a prohibited act, operates in the same manner.

How do tax capital groups work?

Polish tax law allows the creation of tax capital groups for CIT purposes[PGK]. PGK have the status of taxpayers and they are responsible for the taxes.

A PGK may be established by at least two limited liability companies, simple joint-stock companies or joint-stock companies whose average share capital is at least PLN 250 and one of which holds at least 75% of the share capital of the other companies.

The creation of a PGK allows for the summing up of revenues and costs of all companies in the group and their joint settlement of tax. Certain revenues are not subject to consolidation (e.g. dividends).

Is there a minimum corporate income tax in Poland?

The minimum income tax is an annual tax. It covers only companies and PGK (i.e. it does not apply to other legal persons that are CIT taxpayers, e.g. foundations, including family ones, associations).

The tax obligation covers those companies or PGK which in a given tax year incurred a loss from a source of income other than from capital gains or achieved a share of income from a source of income other than from capital gains (specified in the regulations) in income other than from capital gains in the amount of no more than 2%. Both the loss and profitability for the purposes of minimum tax are calculated on special principles.

The minimum CIT tax rate is 10% of the tax base.

The tax base is 3% of revenues other than capital gains revenues or – depending on the taxpayer’s choice – 1,5% of such revenues, additionally increased by selected cost categories.

The regulations contain a number of exemptions from the minimum tax, e.g. in the case of taxpayers starting a business or those whose profitability in the three previous years was at least 2%, companies that are small taxpayers or owned exclusively by individuals, etc.

Exit tax

The following are subject to income tax on unrealized profits:

1. transfer of an asset outside the territory of Poland, as a result of which Poland, in whole or in part, loses the right to tax income from the sale of that asset, while the transferred asset remains the property of the same entity;

2. change of tax residence by a taxpayer subject to tax liability in Poland on all of his/her income (unlimited tax liability), as a result of which Poland loses the right to tax income from the sale of an asset owned by that taxpayer, in connection with the transfer of its registered office or management board to another country, including in connection with a cross-border transformation.

The transfer of an asset outside the territory of the Republic of Poland includes in particular a situation in which:

1. a Polish resident transfers to his/her foreign permanent establishment an asset previously connected with the activity conducted in the territory of the Republic of Poland;

2. a non-resident transfers to the country of his or her tax residence or to a country other than Poland where he or she conducts business through a foreign establishment, an asset previously connected with the business conducted in Poland by the foreign establishment;

3. a non-resident transfers to another country all or part of the business activity previously conducted through a foreign establishment located in Poland.

Income from unrealized gains is the excess of the market value of an asset determined on the date of its transfer or on the day preceding the date of the change of tax residence over its tax value.

The tax rate is 19%.

Tax on shifted income

The tax on shifted income is a tax imposed on Polish taxpayers paying certain types of receivables (e.g. costs of advisory services, market research, advertising services, management and control, data processing, insurance, guarantees and sureties and similar services) to foreign related entities, if these related entities are subject to relatively low taxation or are, for example, obliged to transfer these receivables further.

The tax is 19% of the tax base.

Is there a double taxation treaty in force between Poland and Ukraine?

Polish regulations imposing on CIT taxpayers the obligation to settle the tax should be applied taking into account double taxation treaties [UPO].

Poland and Ukraine are bound by the Convention for the Avoidance of Double Taxation and the Prevention of Fiscal Evasion with Respect to Taxes on Income and on Capital, signed on 12 January 1993.

This agreement is effective from 1 January 1995.

Withholding tax

Withholding tax [WHT] is a flat-rate formula for taxing selected income of non-residents from sources located in Poland.

WHT applies to, among others:

- interest, royalties, remuneration for selected intangible services, entertainment services – the tax rate is 20%,

- sea or air transport – the tax rate is 10%,

- dividends and other income from participation in the profits of legal persons – the rate is 19%.

These rates may be changed by double taxation treaties.

Poland has implemented participation exemptions in relation to dividends, interest and royalties paid to companies based in the EU/EEA.

Capital Gains Tax

Capital gains tax is applied to income from participation in the profits of legal persons and certain financial income. The tax primarily applies to gains from the sale of securities, such as shares or stocks, as well as dividend income.

The tax rate is 19%. It is levied on both income earned in Poland and income earned from foreign entities, with the provisions of the relevant double taxation treaties applying first.